The Waterfall Method: How Families Build Lasting Multigenerational Wealth

How permanent life insurance can turn today's premiums into a lasting legacy for your family.

5/30/2026

One of the most common questions we hear from families thinking about the future is some version of this: how do I pass wealth to my children or grandchildren in a way that actually lasts? Not a lump sum that disappears, not a tax burden that erodes the gift — but something that genuinely grows from one generation to the next. The waterfall method using life insurance is one of the more elegant answers to that question.

It's a strategy that's been used quietly by financially savvy families for decades, and it works precisely because it plays the long game.

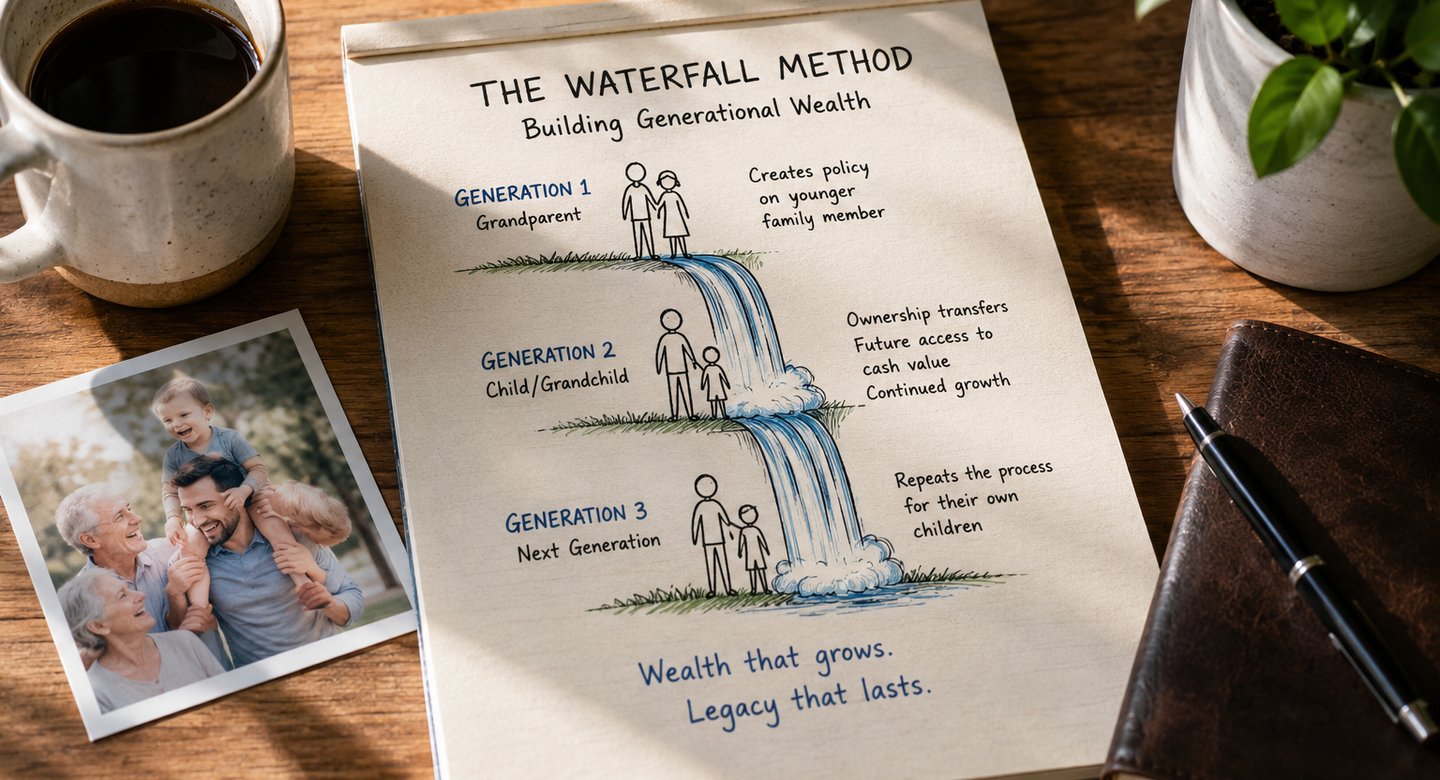

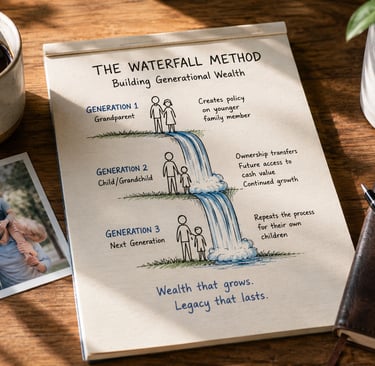

At its core, the waterfall method uses permanent life insurance — typically whole life or universal life — to accumulate cash value over time and pass it down through the generations in a structured, tax-advantaged way. The name comes from the idea that wealth cascades from one generation to the next, compounding as it goes.

Here's how it typically works. A parent or grandparent takes out a permanent life insurance policy on a younger family member — a child or grandchild. Because the insured is young and healthy, premiums are lower, and the policy has decades to grow. The grandparent owns the policy and pays the premiums, which may qualify as annual exclusion gifts under current gift tax rules depending on how the policy is structured. Over time, the cash value inside the policy builds on a tax-deferred basis. Then, when the timing is right, ownership of the policy transfers to the next generation. That person steps in as the new owner, with access to the accumulated value, the ability to continue funding the policy, and eventually the opportunity to do the same thing for their own children.

That last part is what makes it a waterfall rather than a one-time transfer.

A practical illustration helps bring this to life. Imagine a grandparent who begins funding a whole life policy on a newborn grandchild. Over 20 years, the policy quietly accumulates significant cash value. When the grandchild turns 21, ownership transfers to them. They now hold a growing financial asset they can tap for major life milestones — education, a home, starting a business — while a death benefit remains in place for the rest of their life. And when they're ready, they can begin the same process for their own children.

The appeal of this strategy lies in a few distinct advantages. Cash value inside a permanent life insurance policy grows on a tax-deferred basis, and the death benefit is generally received income tax-free by beneficiaries under current tax law. Policy loans can often be taken against the cash value without triggering a taxable event, and in many states, the policy may carry certain asset protection benefits. Life insurance also typically passes directly to named beneficiaries, bypassing the probate process entirely.

Of course, no strategy is without its considerations. Permanent life insurance is a long-term commitment — premiums need to be funded consistently, and surrendering a policy early can result in charges and lost value. Policy loans accrue interest, and if left unrepaid, they reduce the death benefit and can put the policy at risk of lapsing. Transferring ownership between generations may also carry gift tax implications, so working with a qualified advisor on the timing and structure matters. And because the tax treatment of life insurance is based on current federal law, which can change, a tax professional should always be part of the conversation.

The waterfall method tends to resonate most with families who are thinking beyond their own lifetimes — those who want to give the next generation a meaningful financial foundation while still maintaining access to the funds if needed. It's generally less suited for those who need near-term liquidity or prefer higher-growth, market-based investments.

Used well, it's one of the more thoughtful tools available for multigenerational planning.

At Lenhoff Financial, we work with families to evaluate strategies like this within the full context of their financial lives — their goals, their tax situation, their timeline, and the legacy they want to leave. If the waterfall method sounds like it might be worth exploring, we'd love to talk.

This content is for educational purposes only and is not intended as financial, tax, or legal advice.

Get Financial Insights Delivered to Your Inbox

Receive educational content, updates, and ideas designed to help you make more informed decisions for your future.

Helping You Make Informed Decisions

We believe clients should fully understand their options before making an important financial decision. Explore videos covering retirement planning, policy design, tax-advantaged strategies, family protection, and the concepts behind properly structured life insurance solutions.

Lenhoff Financial

Lenhoff Financial Inc.

8540 Executive Woods Drive Suite 501

Lincoln, NE 68512

Contact

Newsletter

Email: info@lenhofffinancial.com

(402) 413-1351

Copyright © 2024 Lenhoff Financial Inc. All rights reserved.